Table of Contents

What’s HOT

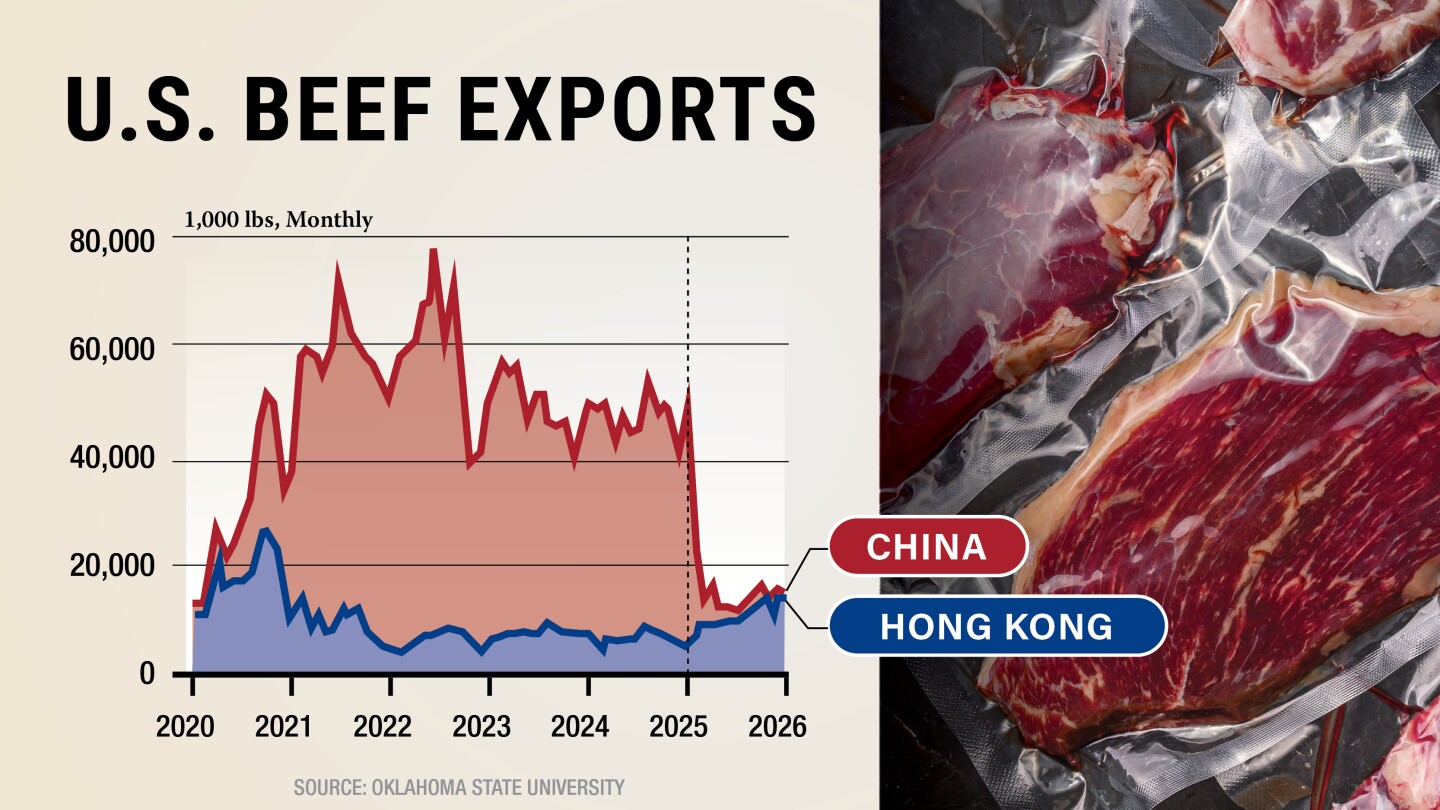

Well… China was HOT Sunday night into Monday’s trade before the market woke up and realized it had little more than a White House press release.

25 MMT of soybeans per year plus another $17 billion in agricultural goods sounds impressive — and on paper would put total purchases near the upper end of the peak Phase One years.

The problem?

The latest agreement is dollar-denominated, anything but specific, and while China has acknowledged the broader diplomatic truce and resumed actions like renewing U.S. beef plant registrations, Beijing has stopped well short of publicly endorsing any large-scale agricultural purchase commitments.

At this point, the market still doesn’t know what China plans to buy, when purchases would occur, or how much of that total actually translates into incremental grain demand versus beef, poultry, and other higher-value products.

Besides, last I checked, we’re still waiting on China to fully fulfill its Phase One commitments.

As mentioned in Sunday’s Weekender, there are few things sexier in ag markets than the idea of China stepping in to buy massive amounts of U.S. corn.

It happened during Trade War 1.0 — but China wasn’t simply buying because of Phase One. They were rebuilding domestic stocks, feeding an expanding hog herd (post-ASF), and taking advantage of the arbitrage opportunity of the century after futures collapsed in 2020.

Fast forward to today and the market has spent months priming itself for a similar story.

Rumors that as much as 30 MMT of China’s 2025 corn crop (10% of production /1.2 billion bushels) suffered weather damage have circulated for months, fueling speculation that China could once again be forced into the world market in a meaningful way.

The last — and really only — time China became a large buyer of U.S. corn was from 2020 into 2022, when they went from virtually nonexistent customer to taking nearly one out of every three bushels exported during the 2020/21 marketing year.

Today, the Dalian-CBOT corn futures spread continues to hover just above $4 per bushel. While it may look like an incredible arbitrage opportunity, the spread remains a far cry from the $6+ levels seen in late 2020 that eventually opened the floodgates for U.S. corn exports.

Keep reading with 14-days free trial

Subscribe to No Bull to keep reading this post and get 14 days of free access to the full post archives.

Start trial